[ad_1]

The U.S. House of Representatives just passed the Financial Innovation and Technology for the 21st Century Act (FIT21), marking a significant milestone in crypto regulation.

What’s the scoop?

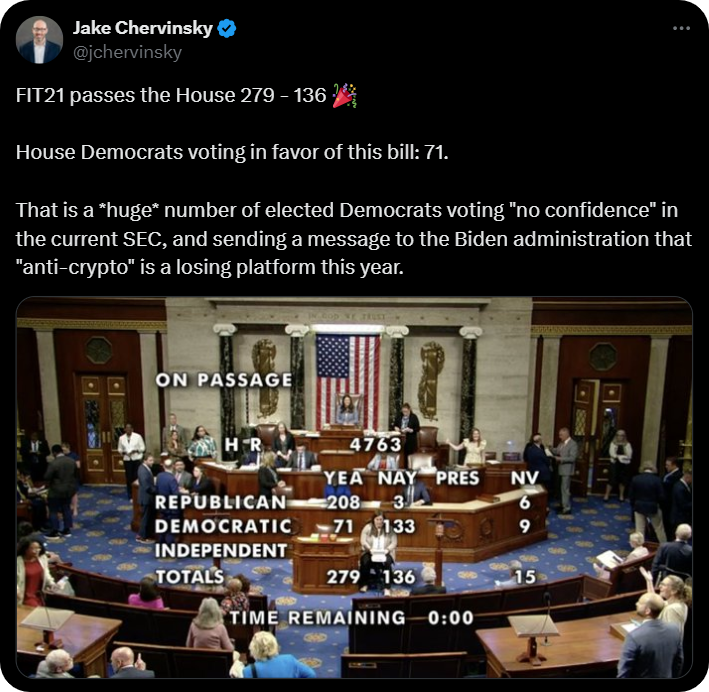

- The House voted 279-136 to approve the bill, with 71 Democrats joining 208 Republicans in favor.

- FIT21 aims to regulate the digital assets market and would empower the Commodity Futures Trading Commission (CFTC) as a key regulator alongside the Securities and Exchange Commission (SEC). The bill also includes consumer protections and provisions for stablecoins and anti-money laundering processes.

- High-profile Democrats, including former House Speaker Nancy Pelosi, supported the bill, highlighting the rising bipartisan tide around crypto regulation.

- Several amendments were considered, with only those by Reps. Brittany Pettersen (D-Colo.) and Ralph Norman (R-S.C.) passing. Pettersen’s amendment expands the Bank Secrecy Act to digital assets, while Norman’s requires a study on foreign-owned digital asset businesses.

Bankless take:

The FIT21 legislation now moves to the U.S. Senate, where its future is uncertain due to a lack of a companion bill and unclear support. Even if FIT21 were to pass the upper house of Congress, it would still be subject to a potential veto by President Biden, who has been critical of the bill but hasn’t confirmed any veto plans yet.

Whatever happens, it’s the first major non-resolution crypto bill approved by the U.S. House, marking a big political win for the crypto industry. The passing of the bill’s first hurdle coincides with a seemingly thawing regulatory environment in the U.S., as Ethereum ETFs seem on the verge of approval and the Senate recently repealed a SEC-backed crypto rule.

If FIT21 does go on to succeed in the Senate, a new era of more sensible American crypto regulation would be decidedly within reach.

[ad_2]

Read More: www.bankless.com

Bitcoin

Bitcoin  Ethereum

Ethereum  Tether

Tether  XRP

XRP  BNB

BNB  Solana

Solana  USDC

USDC  Dogecoin

Dogecoin  Cardano

Cardano  Wrapped Bitcoin

Wrapped Bitcoin  Hyperliquid

Hyperliquid  Wrapped stETH

Wrapped stETH  Bitcoin Cash

Bitcoin Cash  Sui

Sui  LEO Token

LEO Token  Avalanche

Avalanche  Stellar

Stellar  USDS

USDS  Toncoin

Toncoin  WhiteBIT Coin

WhiteBIT Coin  Shiba Inu

Shiba Inu  WETH

WETH  Litecoin

Litecoin  Wrapped eETH

Wrapped eETH  Binance Bridged USDT (BNB Smart Chain)

Binance Bridged USDT (BNB Smart Chain)  Hedera

Hedera  Ethena USDe

Ethena USDe  Polkadot

Polkadot  Coinbase Wrapped BTC

Coinbase Wrapped BTC  Pi Network

Pi Network  Pepe

Pepe  Aave

Aave  Ethena Staked USDe

Ethena Staked USDe  Aptos

Aptos  OKB

OKB  Bittensor

Bittensor  BlackRock USD Institutional Digital Liquidity Fund

BlackRock USD Institutional Digital Liquidity Fund  Jito Staked SOL

Jito Staked SOL  NEAR Protocol

NEAR Protocol  sUSDS

sUSDS