Over $500 million in ENA was just distributed to eligible claimants through Ethena’s first round of airdrops, but contention over the protocol is reaching a fever pitch on Crypto Twitter. Why are two bluechip DeFi protocols now embroiled in conflict over Ethena?

Yesterday afternoon, a governance proposal hit the Maker forum asking delegates to consider increasing the capacity of recently established USDe and sUSDe lending facilities on Morpho from 100 million DAI to 600 million DAI, with the ability to extend the line to up to 1 billion DAI and the majority of funds set to be lent out at relatively high loan-to-value (LTV) ratios of 86% and greater.

Scaling up the Morpho Vault. pic.twitter.com/LmJsfwPXZa

— Sam MacPherson (@hexonaut) April 1, 2024

Maker’s move to increase usage of Ethena’s synthetic dollar stablecoin as collateral is a play to increase DAI adoption and comes amid a marked decline in the market dominance of its stablecoin, which has plunged 20% since the beginning of the year.

In response to Maker’s governance proposal, an Aave contributor launched a proposal of their own, seeking to set the LTV of DAI to 0% across all Aave deployments, removing the ability of users to borrow against DAI as a collateral asset.

The proposal to remove the collateral status of $DAI in Aave is now live.

This will mitigate potential contagion risks for the Aave users.

DAI remains an onboarded asset that users are free to borrow.

“Endgame” it is.https://t.co/71NP8ZMB74 pic.twitter.com/nUssFlpxvQ

— Marc “Chainsaw” Zeller

(@lemiscate) April 2, 2024

Confusing many is Aave’s demonstrated willingness to onboard Ethena’s sUSDe to its V3 Ethereum deployment, with the March 19 temperature check that passed with near unanimous support sharply contrasting with the protocol’s visceral reaction to Maker’s recent efforts to increase lending activities against the token.

While it is possible that DAI lending through Aave could be conducted in a risk-isolated fashion (similar to how future sUSDe markets will likely operate) that would eliminate the potential for contagion, Aave is no longer willing to underwrite the increasing amount of risk that Maker has demonstrated it will assume in the pursuit of bolstering DAI supply and treasury revenues.

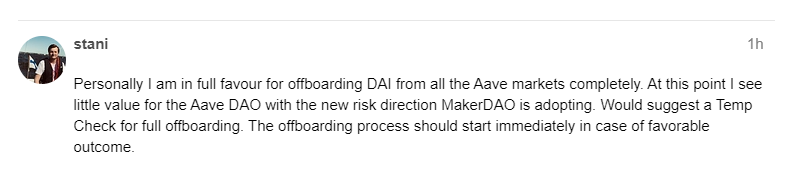

Aave Founder Stani Kulechov reiterated this sentiment, proposing to off-board DAI from all markets completely and stating that he sees “little value for the Aave DAO with the new risk direction MakerDAO is adopting.”

Given the extremely high yields that Ethena’s stablecoins are earning, with sUSDe generating best in-class returns for a stablecoin from funding/staking payments and USDe throwing off tremendous airdrop rewards, demand for leverage on these assets is high and holders are willing to pay a premium to obtain it.

Despite just 2% of circulating DAI supply being collateralized by Maker’s current Ethena lending operations, these loans are earning a 36% annualized return and contributing 10% towards Maker’s expected revenues.

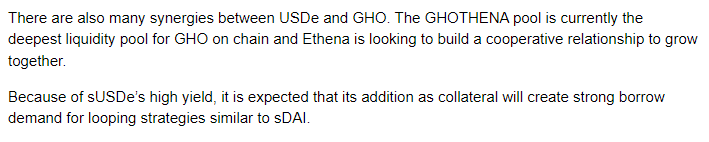

While Maker’s increased adoption of Ethena assets as collateral has undoubtedly increased the risk profile of DAI to some degree, Aave’s retaliatory reaction feels harsh and could be seen as geared toward further supporting GHO – the protocol’s own stablecoin and a direct competitor to DAI – seeing as the potential benefits that Ethena’s integration with Aave could produce for GHO were contemplated in the governance proposal to enable sUSDe markets…

Read More: www.bankless.com

Bitcoin

Bitcoin  Ethereum

Ethereum  Tether

Tether  XRP

XRP  BNB

BNB  Solana

Solana  USDC

USDC  Dogecoin

Dogecoin  Cardano

Cardano  Sui

Sui  Wrapped Bitcoin

Wrapped Bitcoin  Wrapped stETH

Wrapped stETH  Avalanche

Avalanche  Stellar

Stellar  Shiba Inu

Shiba Inu  Hedera

Hedera  Hyperliquid

Hyperliquid  Toncoin

Toncoin  Bitcoin Cash

Bitcoin Cash  Pi Network

Pi Network  LEO Token

LEO Token  Litecoin

Litecoin  Polkadot

Polkadot  USDS

USDS  WETH

WETH  Pepe

Pepe  Wrapped eETH

Wrapped eETH  Binance Bridged USDT (BNB Smart Chain)

Binance Bridged USDT (BNB Smart Chain)  Ethena USDe

Ethena USDe  Coinbase Wrapped BTC

Coinbase Wrapped BTC  WhiteBIT Coin

WhiteBIT Coin  Bittensor

Bittensor  NEAR Protocol

NEAR Protocol  Aptos

Aptos  Aave

Aave  OKB

OKB  Ondo

Ondo  BlackRock USD Institutional Digital Liquidity Fund

BlackRock USD Institutional Digital Liquidity Fund