[ad_1]

Get the best data-driven crypto insights and analysis every week:

By: Parker Merritt

The pseudonymous nature of the Bitcoin blockchain simultaneously offers real-time visibility into the full ledger of transactions, while at the same time posing a difficult challenge of mapping addresses to specific off-chain entities. At one end of the spectrum, a single individual can spin up hundreds of wallet addresses at little or no cost. On the other extreme, centralized exchanges may custody the funds of tens of thousands of users under the control of a single omnibus account.

Despite the difficulty of matching users to addresses, certain segments of the on-chain ecosystem offer more explicit indications of address ownership. Bitcoin miners, in particular, are relatively easy to identify thanks to the heuristic of “0-hop” and “1-hop” addresses. In this week’s issue of State of the Network, we apply this heuristic to follow the flow of funds between mining pools and miners, uncovering hidden links between entities in an effort to quantify the true degree of mining decentralization.

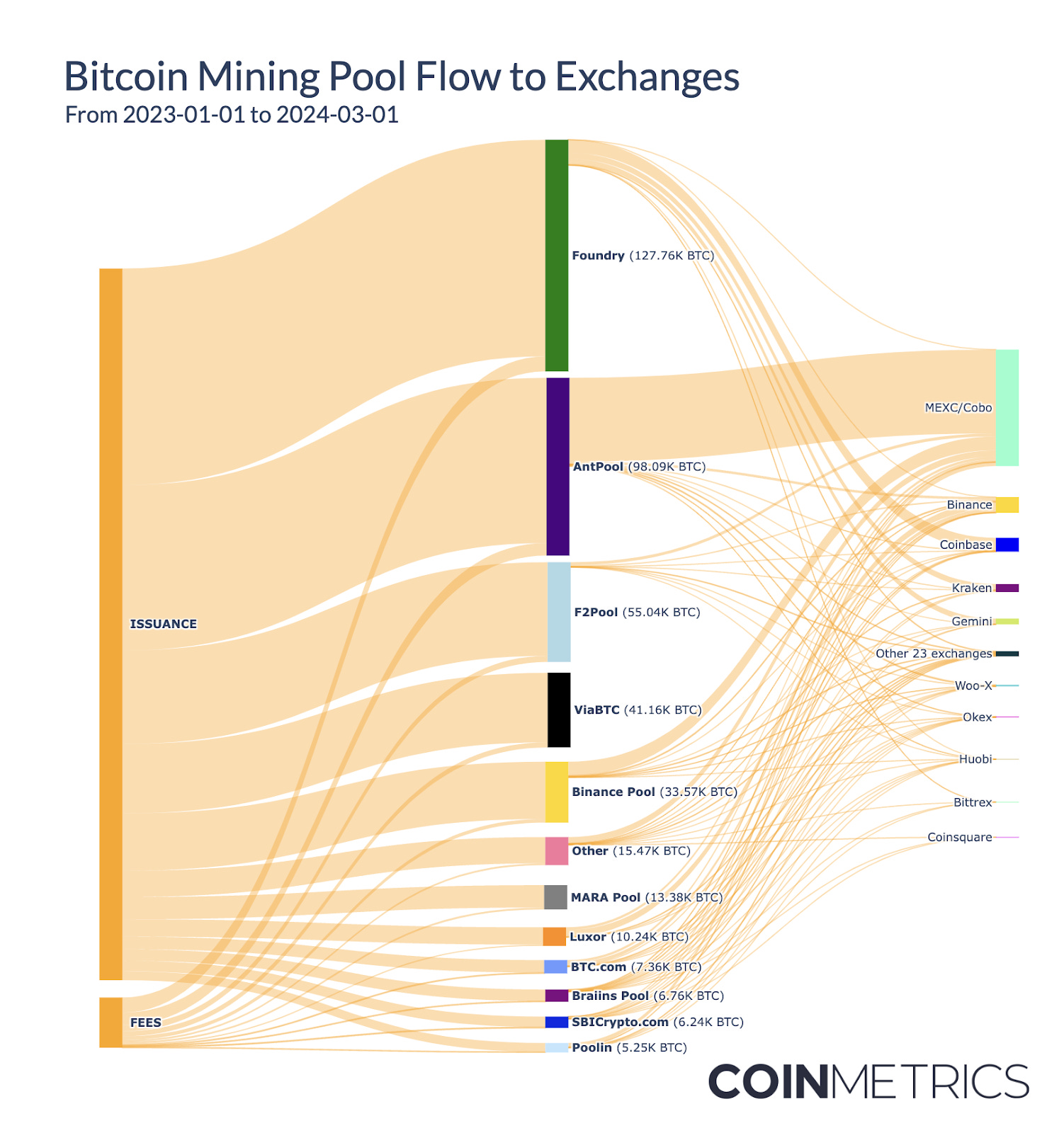

As discussed in previous issues of our Following Flows series, the vast majority of Bitcoin miners direct their hashrate to a service provider called a “mining pool,” allowing them to mitigate the short-term volatility of mining revenue by splitting rewards with other miners. These mining pools are the direct recipients of new BTC issuance, as well as any fees associated with the batch of transactions they append to the blockchain. Due to their unique proximity to new BTC issuance, mining pools are generally identifiable as the owners of “0-hop” addresses.

Furthermore, the majority of mining pools will publicly stamp blocks they mine with a claim of ownership, known as the “coinbase signature.” This on-chain metadata allows us to map 0-hop addresses to their corresponding mining pool, providing a reliable heuristic for tracking the flow of revenue for a coalition of miners. Concentration of hashrate into a handful of powerful pools has been a longstanding concern in the Bitcoin community, and on-chain flows confirm an increasing centralization of power. The top 2 pools— Foundry and AntPool— received 53% of all mining rewards over the course of 2023.

Generally, the link between a cluster of 0-hop addresses and a mining pool is mutually exclusive, with each pool controlling an isolated set of payout addresses. However, some pools have an observable overlap in 0-hop addresses. For example, examining the seven 0-hop accounts associated with Binance Pool and BTC.com, addresses 3L8…8TZ and bc1…9jv have received payouts from both pools.

These periods of overlap are brief, with just 22 BTC.com-stamped blocks directing payouts to Binance Pool-affiliated addresses in February & September 2023. Still, any amount of shared flows lends credence to the theory that Binance Pool is simply a white-label instantiation of BTC.com software, further complicating efforts to directly measure pool centralization.

After taking custody of new Bitcoin rewards (and extracting a small service fee), mining pools distribute earnings from their 0-hop address to their miner constituency. Miners are generally identified via “1-hop” addresses, linked to mining pool addresses by at least one inflow. Historically, the “0-hop” and “1-hop” pattern has been the primary lens through which analysts have understood the relationship between miners and mining pools.

However, there are a few considerations that must be taken into account before making the blanket assumption that all 1-hop addresses are controlled by miners. Some miners withdraw earnings directly to an exchange address, presumably providing the optionality to liquidate BTC and cover short-term operating costs. Unsurprisingly, Binance, Kraken, and Coinbase are among the top beneficiaries of pool outflows, receiving just shy of 21K BTC across the trio. There’s also clear regional alignment between U.S.-based pools and U.S. exchanges, with Foundry making up 89% of the pool deposits to Coinbase, Kraken, and Gemini.

Seychelles-based MEXC—an exchange averaging at $1B in spot volumes daily, or 10% of Binance’s total—initially appears to be a surprisingly high-profile recipient of mining payouts, particularly from AntPool. Other address-clustering sources tie many of the same MEXC-linked addresses to Cobo.com, a Singapore-based custodian headed by F2Pool co-founder Discus Fish. The overlapping address tags underscore the difficult nature of mapping addresses to a single entity. Given the ambiguity of ownership, we’ll call this group of addresses the “MEXC/Cobo cluster.”

Since January 2023, addresses in the “MEXC/Cobo cluster” have received approximately 63.6K BTC in the form of mining pool payouts. AntPool contributed a staggering 45.7K BTC to this sum—nearly 47% of their total mining inflow.

Source: Coin Metrics ATLAS & Tagging API

The majority of the pool-to-exchange flows also contain inputs from multiple pools within the same transaction. Based on the “common input heuristic” (the most popular method for clustering addresses), this transaction structure typically indicates a set of addresses is controlled by the same owner. At the very least, the shared inputs suggest a high degree of coordination between pools when moving funds to exchanges.

Since January 2023, there have been 1,200+ instances of pool-to-exchange flows with shared inputs from multiple pools on a daily cadence. Pools contributing to the transactions include AntPool, Binance Pool, F2Pool, Luxor, BTC.com, Braiins, and Poolin. Notably, the majority of the cross-input transactions appear to include inputs from MEXC/Cobo-affiliated addresses, indicating the entities play a hands-on role in consolidating mining pool outflows and, ultimately, forwarding funds to other exchanges like Binance and WOO X.

Source: Coin Metrics ATLAS & Tagging API

Looking at the remaining 1-hop address set, there’s still a puzzling amount of transfers from multiple mining pools to a singular address, 3BH…WGb. Last December, analysts at TheMinerMag spotted a suspicious consolidation of funds originating from multiple mining pools. In addition to receiving 36.3K BTC from the 2nd-largest pool AntPool, the 3BH…WGb address has received substantial contributions from 7 of the other top mining pools: F2Pool, Binance Pool, F2Pool, Luxor, BTC.com, Braiins, and Poolin. In aggregate, 57.4K BTC flowed from pools to this address, making up around 18% of the one-hop flow total (excluding exchanges) since January 2023.

The 3BH…WGb address doesn’t share inputs with other pools or exchanges, making its ownership difficult to pinpoint via heuristical clustering. Nonetheless, the consolidation of funds into this address implies the existence of an entity backstopping multiple pool operations.

Many of these pools offer a Full Pay Per Share (FPPS) payout model, allowing miners to receive consistent compensation for their hashrate, regardless of whether the pool consistently mines blocks. While convenient for miners, FPPS introduces liquidity risk, as short-term variance in “pool luck” can result in payouts temporarily exceeding the amount of incoming pool revenue. The collapse of Poolin in 2022 was largely attributed to a FPPS imbalance, with the illiquid pool ultimately suspending withdrawals and triggering an 80% exodus in pool hashrate.

Still, the mining pool landscape is fiercely competitive, and pools have had little choice but to embrace FPPS. In November 2022, Riot Platforms (RIOT) publicly broke off their relationship with Braiins, a pool pioneer offering Pay Per Last N Shares (PPLNS). This once-standard payout structure introduces a high level of revenue volatility, forcing miners to stomach short-term variance in pool luck. After a prolonged period of bad luck with Braiins, on-chain flows indicate Riot switched to the more predictable payout model offered by Foundry, the leading FPPS pool. One year later, Braiins Pool announced they would switch to FPPS.

For smaller pools, absorbing the impact of prolonged periods of bad luck requires integrating with a larger, more liquid partner. The 3BH…WGb address appears to be this partner. Incidentally, the address is also a regular recipient of flows from the MEXC/Cobo address cluster, suggesting a broad level of coordination among these entities. The common thread between these businesses is Loop, an “all-in-one assets transfer network,” created by Cobo.

Given the accounting challenges associated with FPPS, it’s likely that mining pools are leveraging Cobo’s Loop Network for liquidity and payout management, resulting in an increasing concentration of flows into a select number of Loop-affiliated addresses. While working with a 3rd-party to manage mining rewards should theoretically help minimize short-term liquidity risk, it also forces miners to take on additional counterparty risk, inserting yet another middleman between miners and their rewards. Though decentralization advocates often note miners can “easily switch pools,” pool participation in this arrangement represents nearly 50% of the Bitcoin hashrate, leaving miners few choices for opting out entirely.

In this analysis, we’ve examined several instances of overlap between pool transactions, from shared 0-hop addresses to common-input pool payouts. Some cross-pool payments can be explained away as byproducts of a shared software stack. Others provide clear evidence that mining pools are coordinating more closely than it appears on the surface.

Mining pool centralization remains a top-of-mind concern in the Bitcoin community. Even at face value, the overwhelming majority of mining rewards being funneled to just two pools (Foundry & AntPool) elevates risk factors like censorship and network disruption. Though the remaining allocation of hashrate is relatively well-distributed among smaller pools, on-chain links between pool addresses warrant concern, pointing towards a hidden consolidation of power in the mining ecosystem.

A special thanks to Ian Descoteaux for his input on this analysis.

Over the past week, Bitcoin’s market capitalization surged by 17%, reaching an all-time high of over $1.3T on Monday, March 4th 2024. Concurrently, the growth of major stablecoins continued, with Tether (USDT) achieving an aggregate supply of $100B for the first time, and USDC reaching $25B in supply. Activity rose across several other ERC-20s, buoyed by a strong week for digital asset markets.

This week’s updates from the Coin Metrics team:

-

Reported Spot Volume across exchanges hit $100B last Wednesday. Follow Coin Metrics’ State of the Market newsletter which contextualizes the week’s crypto market movements with concise commentary, rich visuals, and timely data.

As always, if you have any feedback or requests please let us know here.

Coin Metrics’ State of the Network, is an unbiased, weekly view of the crypto market informed by our own network (on-chain) and market data.

If you’d like to get State of the Network in your inbox, please subscribe here. You can see previous issues of State of the Network here.

© 2024 Coin Metrics Inc. All rights reserved. Redistribution is not permitted without consent. This newsletter does not constitute investment advice and is for informational purposes only and you should not make an investment decision on the basis of this information. The newsletter is provided “as is” and Coin Metrics will not be liable for any loss or damage resulting from information obtained from the newsletter.

[ad_2]

Read More: coinmetrics.substack.com

Bitcoin

Bitcoin  Ethereum

Ethereum  Tether

Tether  XRP

XRP  BNB

BNB  Solana

Solana  USDC

USDC  Dogecoin

Dogecoin  Cardano

Cardano  Wrapped Bitcoin

Wrapped Bitcoin  Hyperliquid

Hyperliquid  Wrapped stETH

Wrapped stETH  Bitcoin Cash

Bitcoin Cash  Sui

Sui  LEO Token

LEO Token  Stellar

Stellar  Avalanche

Avalanche  USDS

USDS  Toncoin

Toncoin  WhiteBIT Coin

WhiteBIT Coin  Shiba Inu

Shiba Inu  WETH

WETH  Litecoin

Litecoin  Hedera

Hedera  Wrapped eETH

Wrapped eETH  Binance Bridged USDT (BNB Smart Chain)

Binance Bridged USDT (BNB Smart Chain)  Ethena USDe

Ethena USDe  Polkadot

Polkadot  Coinbase Wrapped BTC

Coinbase Wrapped BTC  Pi Network

Pi Network  Pepe

Pepe  Aave

Aave  Ethena Staked USDe

Ethena Staked USDe  Aptos

Aptos  OKB

OKB  Bittensor

Bittensor  BlackRock USD Institutional Digital Liquidity Fund

BlackRock USD Institutional Digital Liquidity Fund  NEAR Protocol

NEAR Protocol  Jito Staked SOL

Jito Staked SOL  Ondo

Ondo