Get the best data-driven crypto insights and analysis every week:

By: Matías Andrade & Tanay Ved

-

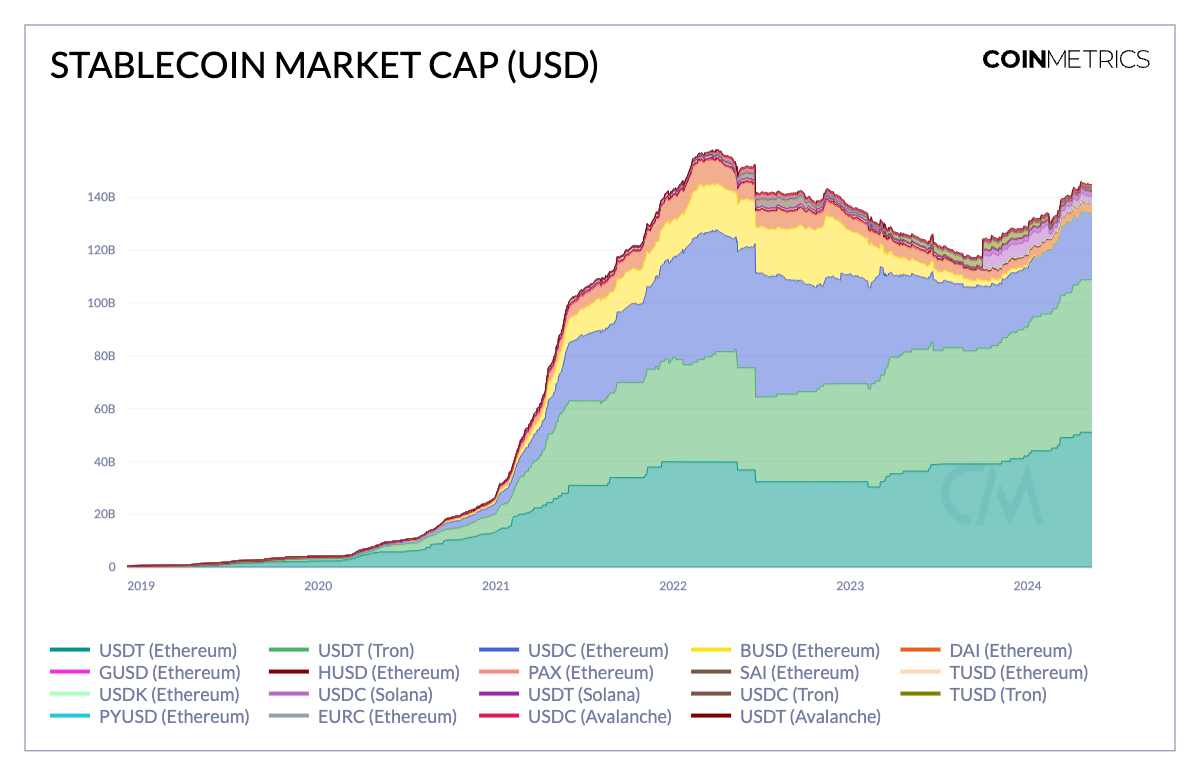

Market Growth: The stablecoin market has grown from below $10B in 2020 to over $160B today, with significant contributions from USDT and USDC.

-

Usage and Adoption: Stablecoins are widely used for transactions, with varying transfer sizes influenced by blockchain transaction fees. Weekly adjusted transfer volume exceeded $50 billion as of April.

-

Global Utility: Analysis of hourly transaction data shows that USDC on Ethereum sees moderate activity around the Hong Kong Stock Exchange (HKSE) and London Stock Exchange (LSE) trading hours. In contrast, USDT on Tron exhibits higher and more evenly distributed transaction activity.

The US dollar has long dominated as the world’s reserve currency. However, this status is now being contested as BRICS countries like China, Brazil and Russia explore alternatives for international trade and central banks diversify their reserves into assets like gold, as opposed to US Treasuries. In contrast, the emergence of stablecoins—digital tokens issued on blockchains, collateralized by fiat currencies, cash equivalents or crypto-assets—are bolstering the demand for US dollars and treasuries across the financial ecosystem.

The adoption of stablecoins is not only pertinent to the US, but also important for dollar-starved economies and emerging markets facing monetary instability or limited access to financial services. Now exceeding a staggering $160B, the market offers a diverse range of stablecoins and supporting infrastructure for both consumer applications such as cross-border payments, and business applications, and exceed all but the top 15 countries’ demand for Treasuries.

In this week’s issue of State of the Network, we assess the growth and usage patterns of stablecoins, providing an in-depth analysis across Coin Metrics’ extensive suite of stablecoin coverage through the lens of our newly developed dashboard.

The global footprint of stablecoins has expanded remarkably, growing from below $10B in total market capitalization in 2020, to over $160B today. While the supply of stablecoins fell in 2023 amid the broader liquidity crunch from central bank tightening and ripple effects of the Terra Luna implosion, the recent rise may be reflective of a renewed demand for crypto assets, buoyed by the launch of bitcoin spot ETFs in the US.

USDT—a fiat-backed stablecoin issued by Tether, continues to maintain its dominance, with $51B (44%) of supply circulating on Ethereum, $58B (52%) on the Tron network with the remaining issued on Solana and Avalanche. Tether’s Q1 2024 attestation revealed a staggering net profit of $4.52B, doubling from the previous quarter. This impressive feat highlights the strength of stablecoin issuer business models like that of Tether and Circle, issuing tokens backed by reserves of low-risk assets like US Treasury bills and cash, while also holding investments like bitcoin or gold that can generate income in the prevailing interest rate environment. As of March 2024, Tether and Circle hold $10 billion and $74 billion, respectively, in US Treasuries as part of their reserves, with Cantor Fitzgerald custodying Tether’s Treasury holdings and BlackRock managing Circle’s reserves within a money market fund.

Source: Coin Metrics Network Data Pro

While Tether, an offshore entity, has capitalized on the regulatory ambiguity in the US which posed challenges to Circle last year, USDC has started 2024 off on a strong footing. Its growth appears to stem from deepened strategic ties with Coinbase, as well as cross-chain expansions to networks like Solana and Ethereum Layer 2’s, improving its market presence and liquidity. Furthermore, Circle’s integration with BlackRock’s BUIDL tokenized fund allowing investors to off-ramp their shares to USDC, are some initiatives that could broaden USDC’s ecosystem and drive greater adoption.

The stablecoin market remains dominated by fiat-collateralized offerings like USDC and USDT, catering to the widespread demand for dollar-pegged assets. The success of established issuers has prompted notable new entrants, such as PayPal’s PYUSD on Ethereum. Crypto-backed stablecoins like MakerDAO’s Dai, collateralized by a basket of crypto-assets and real-world assets (RWAs), have also gained traction. Additionally, synthetic or algorithmic stablecoins like Ethena’s USDe have emerged, employing dynamic hedging strategies to maintain their dollar peg without overcollateralization. This category further consists of stablecoins issued by DeFi protocols, which have become central to their business models, such as Aave’s GHO and Curve’s crvUSD. These varied approaches span a spectrum of reserve backing models, each with its own unique risk and return characteristics.

Source: Coin Metrics Network Dats Pro (Note: The chart does not include stablecoins issued on Ethereum Layer-2’s)

The lion’s share of stablecoin supply—55% or $81B in circulating supply resides on Ethereum today. The most widely adopted and liquid stablecoins gained traction on Ethereum early on, leveraging its security and vast developer base around the Ethereum Virtual Machine (EVM) ecosystem, deepening its network effects.

Tron has also established a strong position in the stablecoin market, capturing a 39% market share, while others like Solana and Avalanche are gaining ground. Attributes like faster transaction speeds and lower transaction fees on chains like Solana are making them attractive for high-frequency and lower value stablecoin use-cases, such as payments as revealed in Stripe’s recent announcement. Similarly, Ethereum layer-2’s like Arbitrum and Base are witnessing stablecoin growth as lower fees drive a shift in cohorts of user activity towards these scalability solutions.

While the burgeoning rise of stablecoins is evident, several questions around the nature of stablecoin usage and adoption remain. For instance, to what extent are stablecoins facilitating real economic value? Are stablecoins being held as a store of value, or being used for transactional purposes? What is the typical size of a stablecoin transfer and what demographics are being served? While these questions are challenging to pinpoint definitively, the transparency of blockchain data can help us better contextualize such patterns in stablecoin activity.

Source: Coin Metrics Network Data Pro

The weekly adjusted transfer volume involving transfers of native units between distinct stablecoin addresses exceeded $50B in April. 48% of this activity stemmed from USDT on Ethereum and Tron, while Dai also saw a record transfer volume of $22B on April 19th. While this metric has seen several spikes, it conveys stablecoins’ utility as a means of settling various forms of economic value.

When transfer volume is viewed relative to its circulating supply, we get a better sense for stablecoin velocity, or the rate at which units are being turned over. However, it’s important to interpret this metric in the right context. USDC on Tron displays the highest velocity, likely due to Circle’s decision to phase out its support which has contracted supply, but increased USDC transfers to other blockchains.

While its supply has declined, Dai notably hit a peak in velocity due to its strong on-chain footprint and growing utilization of the Dai Savings Rate (DSR)—a smart contract effectively functioning as a savings account for deposited Dai. MakerDAO’s governance often implements strategic adjustments to drive usage of Dai, such as the recent hike in interest earned on the DSR. The velocity for USDC on Ethereum and USDT on Tron are currently at similar levels, while USDC is likely to see greater turnover on networks like Avalanche, Solana and Layer-2’s.

Source: Coin Metrics Network Data Pro

We can also discern the extent to which stablecoins are being held as a store of value or being used on-chain by looking at supply held by smart-contracts and externally owned accounts (EOA’s). For instance, while $41B of USDT (Ethereum) is held by EOA’s, its presence in smart contracts has more than doubled since January 2023 to $9.6B. In fact, it now also exceeds USDC in smart contracts by $2.3B. Overall, this indicates stablecoins’ increased role in facilitating transactions on public blockchain infrastructure such as decentralized finance (DeFi) applications, in addition to serving as a store of value or hedge against inflation.

The median transfer value of stablecoins helps contextualize the typical size of a transfer. This metric is highly influenced by the fees and transaction capabilities of the blockchain they are issued on. For instance, USDC and USDT on Ethereum have the highest median transfer values averaging $500 per transfer, to amortize higher transaction fees on mainnet. On the other hand, the median transaction size of USDT on Tron is $230. Similarly, stablecoins on Solana display the smallest transfer value, indicating the prevalence of high-frequency, low-value transfers—a direct consequence of fees being as low as $0.01.

One of the most significant value propositions of stablecoins is their global utility for 24/7 value exchange. Our past analysis on the geographic dominance of stablecoins revealed the preference for USDC usage in North America and Western Europe, whereas USDT has historically seen its highest trading volumes in Asia, Africa and Latin America. However, leveraging 1h transaction data from Coin Metrics ATLAS, we can also discern time-based patterns in activity, revealing hours during which activity is most pronounced.

Source: Coin Metrics ATLAS, Coin Metrics Stablecoin Dashboard

These heatmaps display hourly transaction count activity for USDC on Ethereum and USDT on Tron over the last 3 months, overlaid with major stock market trading hours. USDC activity seems to be relatively dispersed, with moderate activity around Hong Kong Stock Exchange (HKSE) and London Stock Exchange (LSE) trading hours. The most prominent peaks are noticeable around the New York Stock Exchange (NYSE) open and close, suggesting a stronger influence in the US market.

Source: Coin Metrics ATLAS, Coin Metrics Stablecoin Dashboard

On the other hand, transaction activity for USDT on Tron is significantly higher in magnitude, and appears to be more evenly distributed. USDT consistently displays a gradually high concentration of activity starting from the HKSE open, which intensifies during LSE trading hours into the NYSE closing bell. Notably, both stablecoins have seen higher concentration of activity over the past week.

Stablecoins are becoming a vital part of the global financial system, facilitating transactions and serving as stores of value. Their adoption patterns, influenced by blockchain transaction fees, underscore their utility in cross-border payments and DeFi applications. As stablecoins evolve, their significance in the financial landscape will continue to expand. It is imperative to closely monitor their development and integration to fully understand their impact and potential within the financial ecosystem.

Be sure to check out our past research on stablecoins, expanded stablecoin coverage and our comprehensive Stablecoin Dashboard.

This week’s updates from the Coin Metrics team:

-

Coin Metrics is excited to announce our expanded stablecoin and ERC-20 coverage, featuring major and emerging stablecoins on Solana, Avalanche, Tron and Ethereum.

-

Follow Coin Metrics’ State of the Market newsletter which contextualizes the week’s crypto market movements with concise commentary, rich visuals, and timely data.

As always, if you have any feedback or requests please let us know here.

Coin Metrics’ State of the Network, is an unbiased, weekly view of the crypto market informed by our own network (on-chain) and market data.

If you’d like to get State of the Network in your inbox, please subscribe here. You can see previous issues of State of the Network here.

© 2024 Coin Metrics Inc. All rights reserved. Redistribution is not permitted without consent. This newsletter does not constitute investment advice and is for informational purposes only and you should not make an investment decision on the basis of this information. The newsletter is provided “as is” and Coin Metrics will not be liable for any loss or damage resulting from information obtained from the newsletter.

Read More: coinmetrics.substack.com

Bitcoin

Bitcoin  Ethereum

Ethereum  Tether

Tether  XRP

XRP  BNB

BNB  Solana

Solana  USDC

USDC  Dogecoin

Dogecoin  Cardano

Cardano  Wrapped Bitcoin

Wrapped Bitcoin  Hyperliquid

Hyperliquid  Wrapped stETH

Wrapped stETH  Sui

Sui  Avalanche

Avalanche  Stellar

Stellar  LEO Token

LEO Token  Bitcoin Cash

Bitcoin Cash  Toncoin

Toncoin  Shiba Inu

Shiba Inu  Hedera

Hedera  USDS

USDS  WETH

WETH  Litecoin

Litecoin  Wrapped eETH

Wrapped eETH  Polkadot

Polkadot  Binance Bridged USDT (BNB Smart Chain)

Binance Bridged USDT (BNB Smart Chain)  Ethena USDe

Ethena USDe  Pepe

Pepe  Pi Network

Pi Network  Coinbase Wrapped BTC

Coinbase Wrapped BTC  WhiteBIT Coin

WhiteBIT Coin  Aave

Aave  Bittensor

Bittensor  Ethena Staked USDe

Ethena Staked USDe  Aptos

Aptos  NEAR Protocol

NEAR Protocol  OKB

OKB  BlackRock USD Institutional Digital Liquidity Fund

BlackRock USD Institutional Digital Liquidity Fund  Jito Staked SOL

Jito Staked SOL  Ondo

Ondo