Get the best data-driven crypto insights and analysis every week:

By: Tanay Ved & Matías Andrade

The widespread acceptance of cryptocurrencies has evolved significantly in recent times, moving from relative obscurity into the limelight. This shift has been notably propelled by the launch and remarkable performance of Bitcoin spot Exchange-Traded Funds (ETFs), capturing the attention of analysts, bankers, and technologists.

As the landscape of digital assets continues to evolve, the intersection of technology, regulation, and market dynamics presents a complex tapestry for stakeholders. Despite facing regulatory challenges in the United States, where stringent oversight limits direct cryptocurrency custody by banks and financial institutions, the sector’s growth trajectory is undeniable. In this week’s issue of State of the Network, we look at the interplay between the launch of spot Bitcoin ETFs and Coinbase’s recent performance, highlighting their dynamics and broader implications.

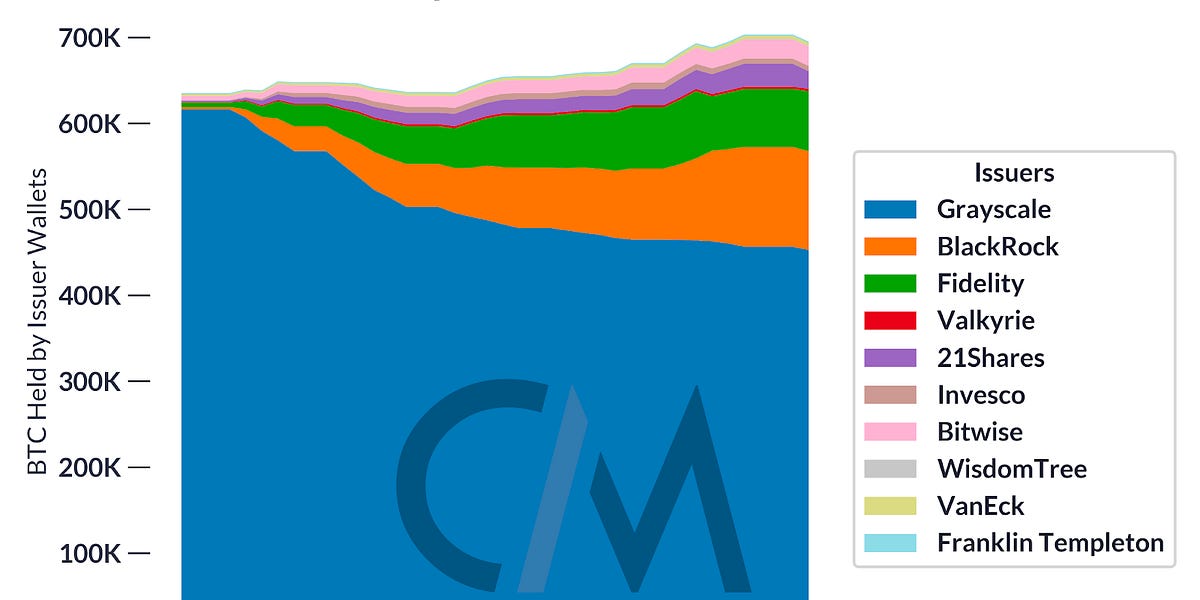

Since the ETFs were approved, we have seen a rapid change in the distribution of BTC between the issuers, with outflows from Grayscale and inflows toward the newly-approved ETFs. One of the reasons for this preference is that the new ETFs have dramatically lower fees compared with Grayscale BTC (GBTC) at 1.5%, with Fidelity and BlackRock at 0.25% (both waiving or reducing fees for an initial period). Another reason is the liquidation of several important holders of GBTC, such as FTX selling approximately $1B and Digital Currency Group’s Genesis investments. Nonetheless, we have seen over $4.8B inflow since the official ETF launch, with over $37B in supply absorbed by exchange-traded products.

In the lead up to the spot Bitcoin ETFs, Coinbase—the largest publicly traded cryptocurrency exchange and the custodian of 8 out of 11 bitcoin ETFs—has been cast under the spotlight. The market has been rife with speculation and divided perspectives regarding the potential impact of these products on Coinbase’s business. Some argue that Coinbase is poised to reap the rewards of an expanded market presence and new revenue channels as the digital asset industry expands, while others argue that the competitive fee landscape of ETFs may deter users from Coinbase, reducing trading volumes and impacting fee revenues. In light of this, Coinbase stands at a pivotal juncture, facing a complex mix of challenges and opportunities amid the rollout of spot ETFs, regulatory battles with the SEC and an increasingly exuberant digital asset market.

In the following section, we will zoom into Coinbase’s financial results, contextualizing our analysis with network and market data to extract key insights from their latest earnings report.

Coinbase published its Q4 2023 earnings last week, reporting a total revenue of $954M—a stellar beat on Wall Street’s expectations of $826M. Diving further into their revenues, they can be broken down into two major drivers: Transaction Revenue and Subscription & Services Revenue, with each category playing a crucial role in Coinbase’s business.

One of the major highlights from the earnings report was the growth in transaction revenue, growing from $322M to $529M, representing a 64% year-over-year increase, comprising 55% of total reported revenue. This rebound is particularly noteworthy since transaction revenue had lagged behind subscriptions and services revenue in Q2 and Q3 of 2023, impacted by compressed trading volumes. The surge was catalyzed by a variety of factors, including the improving of market sentiment and increased risk-on activity in digital asset markets.

Source: Coin Metrics Market Data

Spot trading volume on Coinbase climbed to $3.5B leading up to the ETF launches, matching levels seen in Q4 2022 and only surpassed by the frenzy surrounding Terra Luna’s collapse in the summer of 2022. While both consumer and institutional businesses benefited, retail volumes were a significant contributor in Q4, growing by 163% quarter-over-quarter.

Source: Coin Metrics Market Data

Beyond the composition of trading volumes by user type, another intriguing aspect was the asset breakdown of trading volumes. In Q4, the share of ‘Other’ assets and Tether (USDT) traded on Coinbase grew relative to BTC and ETH. The bucket representing other assets grew by 14% over the quarter, contributing 42% of total trading volume and 57% of transaction revenue. Conversely, the share of BTC and ETH trading volume saw a decrease of 4% and 18% over the year, respectively. This trend not only indicates the current phase of the market cycle, but also highlights the growing influence of consumer-driven volumes reflected in the heightened activity in altcoins like Solana (SOL), Avalanche (AVAX) and other ecosystem related tokens.

Source: Coin Metrics Market Data

This development also raises a crucial question: will the debut of spot Bitcoin ETFs—and the expected introduction of spot Ether ETFs—lead to further compression in trading volume for these assets? While the full effects remain to be seen, a noteworthy trend is the concurrent rise in Binance’s share of BTC volumes following the ETF launches in January. The “Aggregate Volume” section of our weekly State of the Market newsletter can help monitor these dynamics.

While trading activity remains the core facet of the business, Coinbase has expanded its presence in several other verticals. This includes the likes of staking services, stablecoins in conjunction with Circle, Layer-2’s with the introduction of Base and the further monetization of its custody business as a primary custodian for the spot Bitcoin ETFs. Altogether, impressive expansion in these categories has yielded a 33% year-over-year increase in subscription and services revenue, now accounting for 39% of Coinbase’s total revenue mix.

Source: Coinbase Q4 2023 Shareholder Letter

Within this category, revenue from stablecoins has historically been the largest contributor, though it experienced a decline in Q4. These revenues stem from Coinbase’s revenue sharing agreement with Circle, the issuer of USDC stablecoin. Coinbase has garnered substantial income by holding USDC on its platform, with its earnings tied to the circulating supply of USDC and prevailing interest rates—factors that influence the interest income generated on USDC reserves. Despite the dwindling supply of USDC throughout 2023, the adverse effects on revenue have been mitigated by rising interest rates.

Another major avenue of revenue growth has been through “Blockchain Rewards”. This encompasses Coinbase’s staking-as-a-service business, allowing users to stake their assets in order to secure proof-of-stake (PoS) networks like Ethereum, Solana and others. Despite facing regulatory scrutiny from the SEC over its staking business, the blockchain rewards segment grew 53% year-over-year and 28% quarter-over-quarter. This growth can be mainly attributed to ETH staking, reflected by a rise in staked balances, and the growing issuance of Coinbase’s liquid staking token—cbETH, which surpassed 1.4M in supply during Q4. Along with rising asset prices, Coinbase’s 25% commission on ETH staking has significantly enhanced revenue from blockchain rewards.

In addition to its core operations, Coinbase has several emerging segments such as its Layer-2 solution Base, international derivatives exchange and its venture portfolio, which will be realized at fair value following the adoption of FASB accounting standards in Q1 2024. Furthermore, Coinbase is well positioned to capitalize on the sustained inflows into spot Bitcoin ETFs, proving additive to custody fee revenues over the longer term. Overall, Coinbase has navigated the bear market adeptly, reducing its reliance on trading revenues by broadening its business model and revenue streams, while introducing new services with high potential for growth. This strategic diversification, coupled with a proactive regulatory approach and cost reductions, have all boosted its stature in the digital asset landscape.

The first two months have showcased impressive inflows into Bitcoin ETFs, signaling a strong market-wide reception. Alongside, Coinbase’s earnings highlight a strengthened foundation, well poised for future growth. While the longer term implications of the ETFs on Coinbase trajectory are yet to be grasped, their mutual influence underscores positive momentum for the industry. With Bitcoin rising above $1T in market capitalization for the first time since December 2021, growing anticipation around spot Ether ETFs and the forthcoming halving, several indications point towards an exciting period ahead for the digital asset ecosystem.

The market capitalization of Bitcoin and Ethereum expanded further this week, rising by 11% and 13% respectively. Ethereum saw a 10% increase in active addresses, while active addresses on Bitcoin experienced an 8% decline.

This week’s updates from the Coin Metrics team:

-

The Coin Metrics Team will be hosting a Data Challenge at ETH Denver! Learn more about the event & register for it here.

-

Follow Coin Metrics’ State of the Market newsletter which contextualizes the week’s crypto market movements with concise commentary, rich visuals, and timely data.

As always, if you have any feedback or requests please let us know here.

Coin Metrics’ State of the Network, is an unbiased, weekly view of the crypto market informed by our own network (on-chain) and market data.

If you’d like to get State of the Network in your inbox, please subscribe here. You can see previous issues of State of the Network here.

© 2024 Coin Metrics Inc. All rights reserved. Redistribution is not permitted without consent. This newsletter does not constitute investment advice and is for informational purposes only and you should not make an investment decision on the basis of this information. The newsletter is provided “as is” and Coin Metrics will not be liable for any loss or damage resulting from information obtained from the newsletter.

Read More: coinmetrics.substack.com

Bitcoin

Bitcoin  Ethereum

Ethereum  Tether

Tether  XRP

XRP  BNB

BNB  Solana

Solana  USDC

USDC  Dogecoin

Dogecoin  Cardano

Cardano  Hyperliquid

Hyperliquid  Wrapped Bitcoin

Wrapped Bitcoin  Wrapped stETH

Wrapped stETH  Sui

Sui  Bitcoin Cash

Bitcoin Cash  LEO Token

LEO Token  Avalanche

Avalanche  Stellar

Stellar  Toncoin

Toncoin  Shiba Inu

Shiba Inu  USDS

USDS  WETH

WETH  Wrapped eETH

Wrapped eETH  Litecoin

Litecoin  Hedera

Hedera  Binance Bridged USDT (BNB Smart Chain)

Binance Bridged USDT (BNB Smart Chain)  Ethena USDe

Ethena USDe  Polkadot

Polkadot  WhiteBIT Coin

WhiteBIT Coin  Coinbase Wrapped BTC

Coinbase Wrapped BTC  Pepe

Pepe  Pi Network

Pi Network  Aave

Aave  Ethena Staked USDe

Ethena Staked USDe  Bittensor

Bittensor  OKB

OKB  BlackRock USD Institutional Digital Liquidity Fund

BlackRock USD Institutional Digital Liquidity Fund  Aptos

Aptos  NEAR Protocol

NEAR Protocol  Jito Staked SOL

Jito Staked SOL