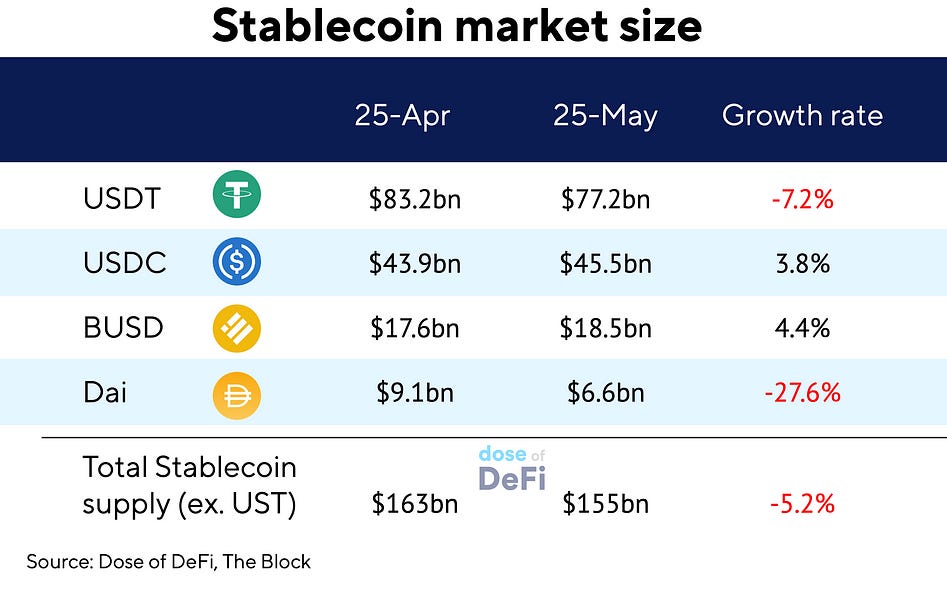

The whir around UST’s death spiral is still echoing through crypto. At a minimum, the saga will dent risk appetite, and will likely soon lead to a US-led regulatory push around stablecoins. There’s been a lot of ink spilled and podcast tape used on the collapse of UST and what it means for the future of DeFi. Among the many repercussions and lessons learned, to us, there is one clear takeaway: the unavoidable necessity of peg management for stablecoins.

At first, stablecoin designers focused on ensuring that a crypto asset was theoretically stable, but soon realized that traders want a stablecoin that can always be traded for its stated value, and not what it should trade at.

This is a lesson that could have been gleaned from traditional finance (TradFi), which has a long history of managing – but more often than not breaking – pegs. When maintained, pegs lubricate investment flows, but even a small deviation can shatter investor confidence.

In DeFi, stablecoins have different approaches to peg management. Below we’ll explore the peg strategies of the major stablecoins and discuss that while Curve enabled new stablecoins to scale, it may not be the ultimate peg management solution. But first, let’s look back at peg management in TradFi.

Like many things in crypto, pegs are not new in finance, but have a long history:

-

Soros breaks the Bank of England. In 1990, the UK joined the European Exchange Rate Mechanism (ERM), which was intended to provide monetary continuity in Europe prior to the introduction of the Euro. The ERM enabled major European currencies to be exchanged for Deutsche Marks within a fixed band, which was enforced by each country’s central bank.

By 1992, the British Pound (GBP) was trading at the lower end of the band. The UK economy was weak and beset by high inflation, but the fixed rate regime of the ERM prevented market adjustments. That is, until George Soros and other currency speculators forced the Bank of England (BoE) to defend the peg by aggressively shorting the pound.

This culminated in “Black Wednesday” when the BoE and the government purchased more than GBP2 billion an hour from their foreign currency reserves and hiked interest rates by 500 bps in a day. Their aim was to protect the peg for the sake of continental unity, but inevitably they relented and allowed the pound to freely float. Soros reportedly pocketed $1.5 billion on the trade.

-

The Baht amongst the 1997 Asian Financial Crisis. A similar story unfolded in Thailand, where the Thai Baht had been pegged to the US dollar since the 1950s. This went swimmingly until the crisis, when exports slowed, the dollar strengthened as the Fed raised interest rates, and all of the “hot money” from foreign investors suddenly raced for the exits. The Thai Central Bank burned through its foreign reserves, and with contagion spreading to other currencies which did not have the foreign reserves to plug the investment outflows, the bank was forced to let the…

Read More: doseofdefi.substack.com

Bitcoin

Bitcoin  Ethereum

Ethereum  XRP

XRP  Tether

Tether  BNB

BNB  Solana

Solana  USDC

USDC  Cardano

Cardano  Dogecoin

Dogecoin  Pi Network

Pi Network  Wrapped Bitcoin

Wrapped Bitcoin  Hedera

Hedera  LEO Token

LEO Token  Wrapped stETH

Wrapped stETH  Stellar

Stellar  Sui

Sui  Avalanche

Avalanche  USDS

USDS  Bitcoin Cash

Bitcoin Cash  Shiba Inu

Shiba Inu  Litecoin

Litecoin  Toncoin

Toncoin  Polkadot

Polkadot  MANTRA

MANTRA  WETH

WETH  Hyperliquid

Hyperliquid  Ethena USDe

Ethena USDe  Wrapped eETH

Wrapped eETH  WhiteBIT Coin

WhiteBIT Coin  Aptos

Aptos  NEAR Protocol

NEAR Protocol  Ondo

Ondo  sUSDS

sUSDS  Aave

Aave  Pepe

Pepe  Gate

Gate  OKB

OKB  Official Trump

Official Trump  Coinbase Wrapped BTC

Coinbase Wrapped BTC