As DeFi users started shifting away from the Ethereum mainnet to lower-cost chains, the infrastructure need for bridges escalated. While some had already launched at this point, most were still in the research phase. Since then, bridges have multiplied in number, size and scale – and we can now draw conclusions on the market share winners and strategic successes. These industry leaders form the center battlefield for the multichain world that we wrote about last fall – and will be reflecting on later this year. For now, Denis takes a closer look behind the scenes.

– Chris

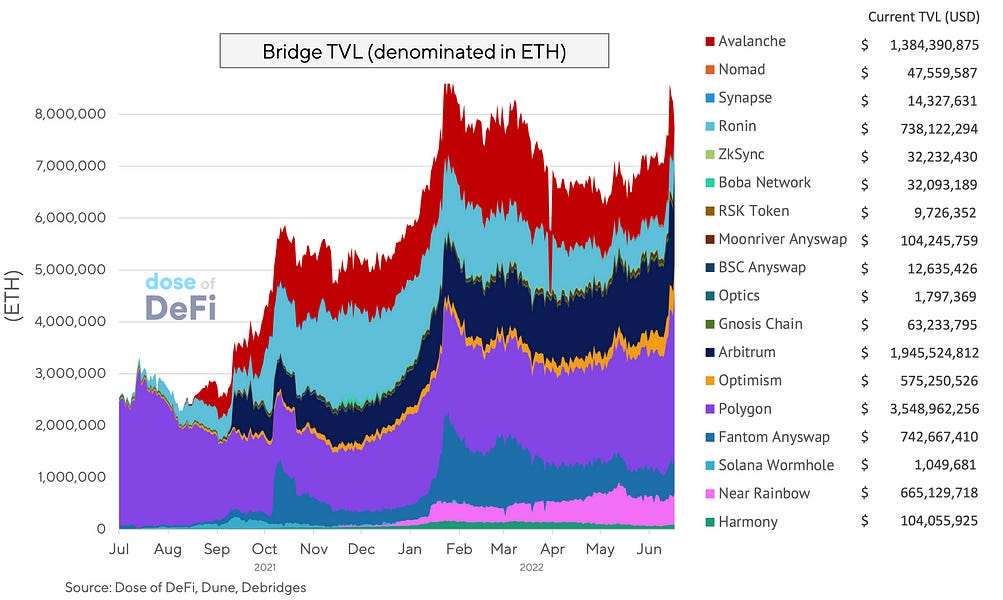

The bridge industry has matured quickly. Following the proliferation of bridges over the last nine months, they now collectively represent roughly 10% of TVL in smart contracts (based on data from the Dune Analytics dashboard by Eliasimos and DefiLlama). To put this rapid growth into context, Polygon Bridge’s USD4 billion TVL is now second only to the TVLs of DeFi giants Curve and Maker.

Taking a step back, bridges were first conceptualized following the emergence of the second blockchain, which prompted discussions on how to connect them. WBTC was the first successful bridge, linking together the two most important blockchains, albeit through a centralized entity. Then things stepped up a gear in late 2021, with the start of an intense era of new bridge production. This article by Dmitriy Berenzon from 1kx gives a detailed overview of this turn of events.

Fast forward nine months, and we’ve now reached a point where the average DeFi investor is using bridges regularly. At face value, this is great news for the swaves of recently-launched bridge projects. However, with the reality of the current market decline and its impact on volumes, these projects are now scrambling for market share among a dwindling set of users.

Amid this scramble, the choice of approach in both bridging and validating methods will be key to determining the bridging competitive landscape in a few years time.

As a basic definition, a bridge facilitates the migration of assets from chain A to chain B. Within this concept, there are generally only two types of assets that a user receives after migration: an asset “IOU” or a natively-issued asset. From the perspective of bridge designers, this equates to one of two methods: token wrapping or creating liquidity.

-

Token-wrapping bridges (combined TVL: USD11.2 billion)

Alternative Layer 1s and their DeFi projects initially saw bridging as a way to bring assets to their ecosystems. Yet creators of these assets weren’t necessarily interested themselves (Avalanche won’t issue an AVAX on a competitor chain, for example). So in such cases, a “wrapper” bridge is used by the Layer 1.

With wrapper bridges, an asset is locked on chain A and a “wrapped” version is minted on chain B. While it may be easier to think in terms of transfers, the asset doesn’t actually move. It’s thus important to instead call it “wrapping” because it’s…

Read More: doseofdefi.substack.com

Bitcoin

Bitcoin  Ethereum

Ethereum  XRP

XRP  Tether

Tether  Solana

Solana  BNB

BNB  Dogecoin

Dogecoin  Cardano

Cardano  USDC

USDC  Avalanche

Avalanche  Shiba Inu

Shiba Inu  Toncoin

Toncoin  Stellar

Stellar  Wrapped stETH

Wrapped stETH  Polkadot

Polkadot  Wrapped Bitcoin

Wrapped Bitcoin  Bitcoin Cash

Bitcoin Cash  WETH

WETH  Sui

Sui  Hedera

Hedera  Litecoin

Litecoin  Pepe

Pepe  NEAR Protocol

NEAR Protocol  LEO Token

LEO Token  Wrapped eETH

Wrapped eETH  Aptos

Aptos  USDS

USDS  POL (ex-MATIC)

POL (ex-MATIC)  Artificial Superintelligence Alliance

Artificial Superintelligence Alliance  Ethena USDe

Ethena USDe  Bittensor

Bittensor  Render

Render  Filecoin

Filecoin  Algorand

Algorand  Arbitrum

Arbitrum  Cosmos Hub

Cosmos Hub  WhiteBIT Coin

WhiteBIT Coin  Immutable

Immutable  Celestia

Celestia